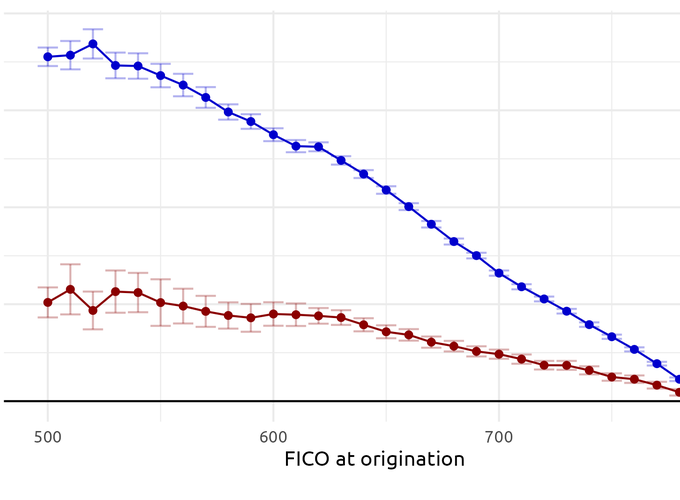

We use 70 million policies linked to mortgages and property-level disaster risk to show that credit scores impact homeowners insurance premiums as much as disaster risk. Homeowners with low credit pay 24% more for identical coverage than high–credit score homeowners. Leveraging a natural experiment in Washington State, we find that banning the use of credit information considerably weakens the relationship between credit score and pricing. We discuss the role of credit information in pricing and show that, although insurance is often overlooked in discussions of home affordability, a low credit score increases premiums roughly as much as it raises mortgage rates.

Figure by Joakim A. Weill

Figure by Joakim A. Weill